Google Cloud Hits $20B, Alphabet Crosses $109B in Revenue — But Constraints, Subscriptions, and YouTube Tell the Real Story:

The 350 Million Club: How YouTube Premium and Google One Became Alphabet’s Secret Weapons.

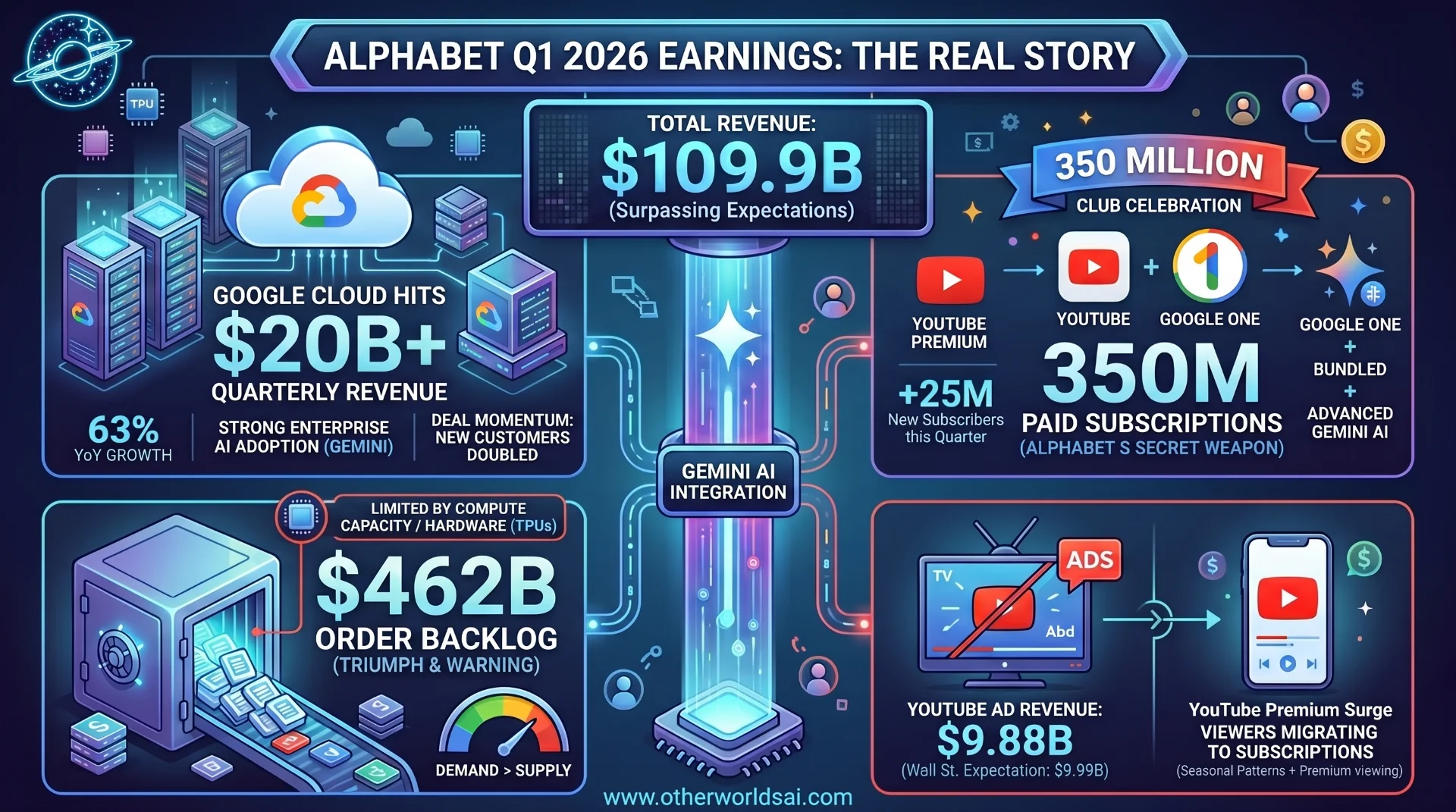

Alphabet just delivered one of its most consequential earnings reports in years — and the numbers are impossible to ignore. In the first quarter of 2026, the parent company of Google posted total revenue of $109.9 billion, handily surpassing Wall Street expectations. The headline grabber: Google Cloud crossed $20 billion in quarterly revenue for the first time, marking a staggering 63% year-over-year increase.

But beneath the record-breaking figures lies a more nuanced story — one of extraordinary demand, supply constraints, evolving subscription growth, and a YouTube business caught in a fascinating structural shift.

Google Cloud Crosses $20B: What's Driving the Record-Breaking Growth

Google Cloud's blockbuster quarter didn't happen by accident — it was powered by a surge in enterprise AI adoption. Alphabet CEO Sundar Pichai told analysts on the Q1 2026 earnings call that the growth was driven by "strong demand" for Gemini Enterprise and its broader AI solutions suite.

The Google Cloud Platform — which encompasses infrastructure, data analytics, AI/ML tools, and Google Workspace — grew at an even faster rate than the Cloud division's overall revenue growth, underscoring just how central enterprise AI has become to Alphabet's business.

The AI-powered products within Google Cloud are growing at a breathtaking pace. Products built on Google's generative AI models grew nearly 800% year-over-year — a figure that, even adjusted for a small base, signals a genuine inflection point in enterprise adoption. Gemini Enterprise paid monthly active users grew 40% quarter-over-quarter, and AI token consumption via the Google API surged from 10 billion tokens per minute in Q4 2025 to 16 billion tokens per minute in Q1 2026. These are not vanity metrics — they reflect real workloads running at real scale.

Deal momentum is also accelerating dramatically. Pichai highlighted that new customer acquisition doubled year-over-year, and the number of deals in the $100 million to $1 billion range also doubled year-over-year, with the company signing multiple "billion-dollar-plus" contracts. Existing customers are outpacing their initial spending commitments by 45% quarter-over-quarter — a powerful signal that once enterprises are in the Google Cloud ecosystem, they're expanding aggressively.

The $462 Billion Backlog: Constrained by Capacity, Not by Demand:

Perhaps the most telling detail in the entire earnings report isn't the revenue — it's the backlog. Google Cloud's order backlog doubled in Q1 2026 to $462 billion, a figure that is both a triumph and a warning. It demonstrates that demand for Google Cloud's services — particularly its TPU hardware, AI infrastructure, and data center capacity — far exceeds what the company can currently deliver.

Pichai was candid with investors about the challenge this creates. "Obviously, we are compute constrained in the near-term," he said. "Our cloud revenue would have been higher if we were able to meet that demand." This is a remarkable admission from the CEO of one of the world's most valuable companies: Google Cloud's growth is not being limited by its sales team, its product quality, or market interest. It's being limited by the physical infrastructure needed to deliver services at scale.

The company's response to this constraint is measured and capital-disciplined. Rather than simply throwing money at the problem, Pichai explained that Google evaluates its investments through the lens of return on capital investment (ROIC) — a framework that helps ensure new spending in TPU production, data centers, and cloud capacity is deployed efficiently. The company expects to work through 50% of its $462 billion backlog over the next 24 months, which, if achieved, would translate into hundreds of billions in future revenue.

350 Million Paid Subscriptions: Google One and YouTube Premium Lead the Charge:

While the cloud numbers dominated the conversation, Alphabet's subscription business quietly posted its own impressive milestone. The company added 25 million new paid subscriptions in Q1 2026, bringing its total to 350 million paid subscribers across its services — up from 325 million in Q4 2025. The growth was led by YouTube Premium and Google One, the company's cloud storage and premium subscription platform.

Google One has become a Trojan horse for Gemini adoption in the consumer market. Access to advanced Gemini AI features is now bundled directly into Google One plans, meaning that as Google One grows, so does the installed base of Gemini users. The company did not disclose specific Gemini subscriber numbers or monthly active user counts, but noted that its prior benchmark of more than 750 million Gemini users — reported in Q4 2025 — likely still holds, as no updated figure was offered.

The Hidden AI War

Nobody Is Telling You About

Our latest documentary deep-dive into the geopolitical struggle for machine intelligence dominance. Explore the two paths of AI development: open source vs. closed architecture.

The enterprise Gemini story is stronger and more transparent. Paid monthly active users of Gemini Enterprise grew 40% quarter-over-quarter, reinforcing the narrative that Google's most committed AI users are businesses — companies deploying Gemini at scale for productivity, automation, and infrastructure. The consumer-to-enterprise pipeline is a core part of Alphabet's AI strategy going forward.

YouTube's Bittersweet Quarter: Ad Revenue Misses, Subscriptions Surge:

**YouTube's Q1 2026 results tell a story **that is both encouraging and instructive for the future of digital media. The platform brought in $9.88 billion in ad revenue, an 11% year-over-year increase — but Wall Street had expected $9.99 billion, and the miss sent a signal that investors can no longer evaluate YouTube's health through ad revenue alone.

The shortfall is a direct consequence of YouTube's own subscription success. As more viewers migrate to YouTube Premium — paying monthly fees for an ad-free experience — they generate subscription revenue instead of ad impressions.

Anthropic’s Surprise Double Launch Directly Targets OpenAI and Google’s AI Dominance

This structural shift was anticipated by Pichai, who warned analysts last quarter that YouTube should be assessed on a combined ads-plus-subscriptions basis. Last year, YouTube's annual revenue topped $60 billion across both streams, with Q4 2025 alone delivering $11.4 billion in YouTube ad revenue. The dip to $9.88 billion this quarter reflects seasonal patterns as well as the continued migration to premium viewing.

Support our research

Independent analysis fueled by you.

This is a bet that Alphabet appears willing to make deliberately. A viewer paying YouTube Premium is more predictable, more loyal, and likely more valuable over a lifetime than an ad-supported viewer.

The trade-off — lower ad revenue today for stronger subscription revenue tomorrow — is one that streaming giants like Netflix pioneered years ago. YouTube is now navigating that same transition, at a scale no other video platform has matched.

Alphabet's Broader AI Strategy: Infrastructure, Gemini, and the Long Game:

Zoom out from the individual numbers, and Alphabet's Q1 2026 results paint a vivid picture of a company in full transformation. Across Google Cloud, Google One, YouTube Premium, and Gemini, the company is executing a unified strategy: embed AI into every product, monetize through subscriptions and enterprise contracts, and invest aggressively in the AI infrastructure — TPUs, data centers, and cloud capacity — needed to sustain that growth for years to come.

The $462 billion backlog is perhaps the most powerful proof point of this strategy's resonance. It means enterprises around the world have already committed, in writing, to spend nearly half a trillion dollars with Google Cloud. The constraint isn't interest — it's compute capacity.

And Alphabet is investing at scale to close that gap, with Pichai emphasizing the company's "robust, long-range planning framework" and its confidence in the "extraordinary opportunities ahead."

For investors and industry watchers alike, the message from Alphabet's Q1 2026 earnings is clear. The AI economy is real, it is large, and it is accelerating faster than the infrastructure needed to support it.

Google — through Gemini, Google Cloud, and its proprietary TPU hardware — is positioned at the center of that opportunity.

The stock responded accordingly, rising after hours as investors digested a report that, despite a YouTube ad miss, demonstrated that Alphabet's AI-first transformation is firmly on track.